When I wrote my first articles on the digital economy in 2016, many economists were writing about a “productivity puzzle.” This article explores the role of ICT in those changes. The introduction can be found here. Additional articles on the relationship between job skills & automation (on demand, retraining, and policy goals) can be found in the links.

Industry concentration and the rise of “superstar firms”

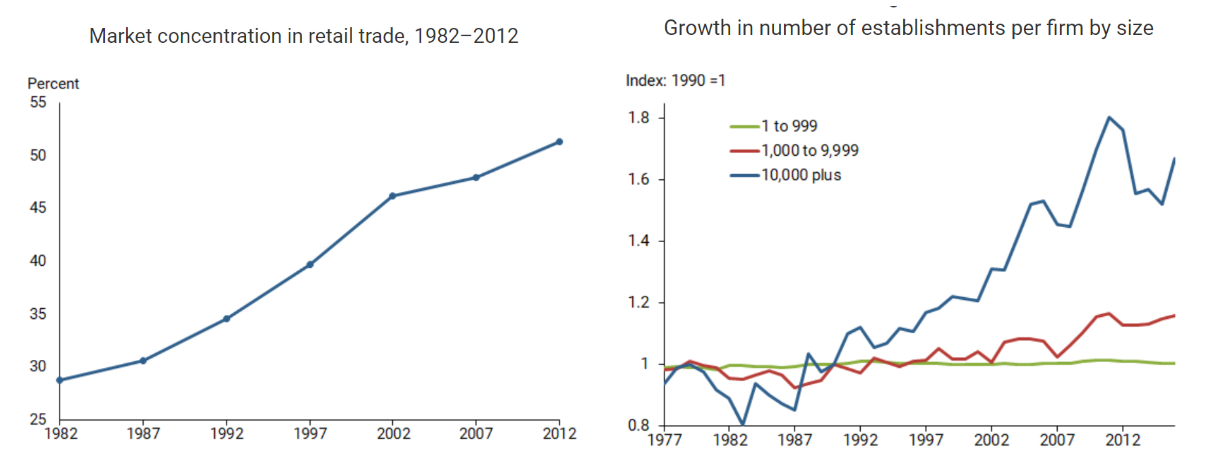

Over the last ~30 years, most industries in the US economy have seen a rising concentration of sales to the largest firms, as well as large geographic expansion of the largest firms.

A recent paper by the SF Fed hypothesizes that this rise in industry concentration is due to effective application of IT - that is, that innovation in ERP, SCM, CRM, FPA, etc. software has allowed the largest firms to expand geographically while retaining their ability to execute effectively.

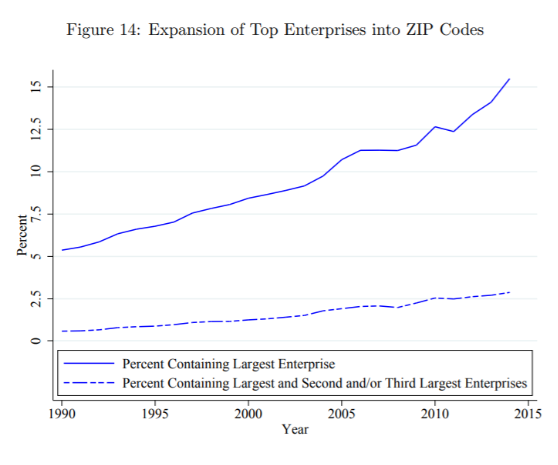

A Richmond Fed analysis on the same topic explores how this geographic expansion (and resulting concentration) has disproportionately favored the largest company in an industry. Over the last 30 years, the largest company has expanded much more rapidly than the #2 and #3 players - often, in local markets, the national leader is competing with smaller regional firms, not their national peers.

The team was surprised to find that, in their analysis, large enterprises do not enter and dominate the local market but instead lower its concentration, either by competing with the previous local monopolist or by simply adding one more establishment that grabs a proportional market share from other local establishments.

This IT expansion, national concentration, and local competition may be linked to the current low pace of growth through two steps (Aghion et al. (2019)): first, the IT expansion increased local competition, and second, increased competition eventually deterred innovation. Those that have innovated effectively have done so in a way that have challenged their competitions’ profit, making it even riskier to invest in innovative activities. These conclusions have prompted the economist Tim Taylor to ask:

- Are these dynamics a result of weaker firms’ inability to make productivity-related improvements (perhaps because they lack organizational or human capital needed to do so)?

- Or do these firms lack incentives to make such investments (perhaps because it is hard for firms to be confident of earning a profit on such investments)?

From this perspective, one might conclude that the decline in productivity is a result of differentiation in firms’ business strategy. However, this has always been the case - why does the modern economy have a resultant drag in productivity relative to times prior?

The role of banking in the productivity puzzle

Could weak productivity be a result of weak businesses staying alive longer? Current research indicates this may be true. In 2018, the Bureau for International Settlements did an analysis on “zombie companies” - those that create enough cash to pay the interest of their debt, but not the principal. Analyzing across 14 advanced economies, the share of “zombie companies” rose, on average, from around 2% in the late 1980s to ~12% in 2016.

How can corporate zombies survive for longer than in the past? They seem to face less pressure to reduce debt and cut back activity. The literature has identified weak banks as a potential key cause (Caballero et al (2008)). When their balance sheets are impaired, banks have incentives to roll over loans to non-viable firms rather than writing them off. Another potential, more general factor is the downward trend in interest rates. Mechanically, lower rates should reduce our measure of zombie firms as they improve ICRs by reducing interest expenses, all else equal. However, low rates can also reduce the pressure on creditors to clean up their balance sheets and encourage them to “evergreen” loans to zombies (Borio and Hofmann (2017)).

This has also been explored in conferences by the OECD (eg, “Weak Productivity: The Role of Financial Factors and Policies”). Here, it was acknowledged that lower rates could have played an unintended role in slowing the cleansing effect of the crisis - for example, by lowering the productivity thresholds afforded by the low interest rate environment. At the same time, conference leaders indicated that early normalization of monetary policy to boost productivity would not pass a cost benefit test—the costs are well-known (lower output, higher unemployment, risks of de-anchoring inflation expectations) and would be large, while the benefits (enhanced resource allocation) are highly uncertain and may be quite small.

It is my belief that, through advances in data and analytics, these dynamics may continue (and might accelerate) in the coming years. New, more productive ways of operating, are being developed - by the already successful superstar firms. (Edit: This is the topic of my friend Alex’s new book). In addition, any recessionary activity will likely be exacerbated by increased firm exits, particularly as interest rates are already at all time lows.

Wage dispersion’s part in the productivity puzzle

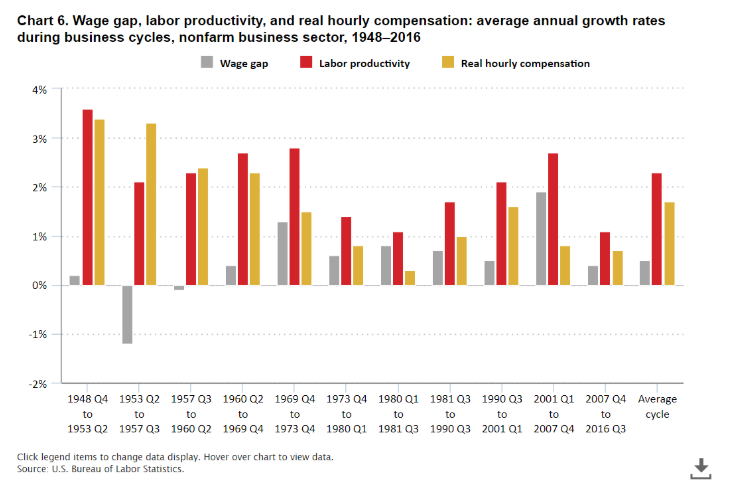

Inequality and its effect on aggregate productivity is one broad problem in our economy. Another is stagnating wages. Even with declining productivity - at lows relative to a historical norm - real hourly compensation has not kept up. In all business cycles since 1970, hourly compensation has not kept pace with gains in labor productivity.

This has also been a significant area of research, with the leading hypothesis that this is another product of the “superstar firm” effect. If technological changes or trade integration push sales towards the most productive firms in each industry, product market concentration will rise as industries become increasingly dominated by superstar firms, which have high markups and a low labor share of value-added. These trends affect wage dispersion (more negatively impacting low-skill workers):

- Technology. Technological change appears to contribute to rising wage inequality. With given endowments of low and high-skilled labour (whose stock can be adjusted only slowly over time), technological change can raise wage inequality if it complements high-skilled workers but substitutes for low-skilled workers. Technological gains are also not equal between firms within an industry - contributing to an inequality of opportunity - which can be reflected in wages.

- Trade Integration. Trade integration also appears to play a role in increased wage inequality. At the aggregate level, the ratio of median to average wages is negatively associated with value added imports. Evidence from micro-aggregated data further suggests that between-firm wage dispersion increased in sectors that became more open to trade (Berlingieri et al., 2017)

Dean Baker postulates that “…much of the story is endogenous in the sense that a weak labor market forces workers to take low pay and low productivity jobs. In fact, adjusting labor wages for the price of the products they produce can account for a large portion of the wage gap. This does not imply that technological change and increased trade integration harm workers, since a large body of evidence suggests that these developments raise aggregate productivity.

Policy redress to promote a well-diversified economy

Over the last 30 years, the basis of competition has been changing and ICT has increasingly become a competitive advantage. More than the technology itself, “superstar firms” create intangible capital - e.g., the ability to organize themselves and design processes that becomes the basis for increased productivity. This should be celebrated!

At the same time, it’s imperative that public policies support the broader creation and sharing of these opportunities. A few potential areas to start could be:

- Greater investment in the “commons,” which is a set of shared resources that every business needs in order to be productive: an educated populace, pools of skilled labor, a vibrant network of suppliers, strong infrastructure, basic R&D and so on

- Restrengthening institutions and bargaining power, which can promote the transmission of productivity gains to wages and typically takes place at the industry level. This may allow workers to appropriate industry-specific rents with minimal impact on capital-labour substitution

- Review tax and transfer systems to account for an increase of gains to capital investment relative to labor investment

- Reform in exit policies (e.g., insolvency regimes) to support the assets and workers associated with low or unproductive firms

- Revised active labor market policies to preserve the labour market attachment and skills of workers who may transition their jobs

It is important to consider that tradeoffs exist for policymakers when considering limiting the growth of large firms. We want to both celebrate success and support future growth. For example, on one hand, curbing the expansions of large firms can be detrimental to growth in the short run because large firms may be able to provide goods and services at a lower cost. However, curbing their expansions may also sustain profit margins that provide incentives for innovation and stimulate growth.

My goal in putting this together was to clarify my own thinking - and to present it in a way that can be challenged and deepened by others. I would be grateful to learn what may resonate (or differ) from your personal perspectives and work.