These articles are part of exploration that started in late 2015 and early 2016. It was a confusing time: autonomous vehicles and Boston Dynamics were frequently in the news and OpenAI was just formed to make sure that the “march towards AGI was safe.” UBI was actively being discussed by Sam Altman and Ray Kurzweil was promoting 10x / exponential thinking. At the same time, economists like Robert Gordon were arguing that we were actually living in a time of low progress.

I tried to develop my own perspective on what was happening, with key conclusions presented at this link. Greater detail supporting other conclusions can be found in Part II and Part III.

Innovation is not improving quality of life as quickly as experienced in prior generations.

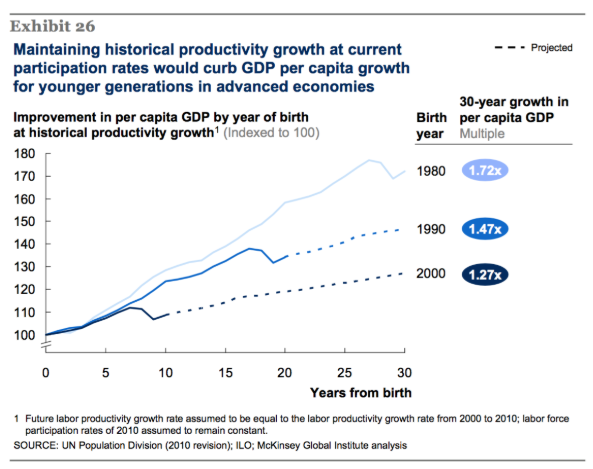

Digitization has had a profound effect on how we live our lives. It has enabled business model innovations (e.g., e-commerce, SaaS) and redefined how we consume media and interact with one another. At the same time, economists believe we may be living in a time in which the net rate of progress is lower than that of prior generations (see chart below; source McKinsey). What explains this apparent paradox?

One thesis for this may be that gains in the technology sector have not effectively led to similar innovation in other sectors of the economy. With this, gains in technology alone cannot have a large influence on overall US economic performance: it only represents ~7% of total GDP.

The performance of US productivity would support this claim. Gains in GDP are divided into two measurements: productivity and labor employment. Productivity, as a rough measure, is the difference between GDP growth and changes in labor employment. For example, in 2014, labor employment grew by 1.7% and GDP grew by 2.4%; “productivity” grew by the difference, 0.7%. Productivity is considered to be a proxy for innovation, as it should account for excess value that workers create (relative to historical performance). In the United States, over the last 40 years, this measure of productivity has slowed. In fact, the rate of productivity growth from 2011 to 2015 was the slowest since the five-year period ending in 1982.

Economists have been trying to figure out this puzzle for many decades, and it is becoming increasingly important. We know that the slowdown across countries is not correlated with IT production or use, suggesting that the problem is not mismeasurement related to IT goods or services. We also know that the slowdown has been broad-based across industries and would be similar if industry weights were held fixed — it does not reflect a rising share of slow-growth industries.

Robert Gordon, an economist, has a theory that, with regard to innovation, the years from 1870-1970 are unparalleled throughout history and advances in ICT in recent decades simply do not compare to the relatively concurrent inventions of electricity, the internal combustion engine, modern sanitation and plumbing, aviation, pharma products, etc. Coupled with this, ICT advances haven’t made the type of broad-based improvements to the economy that these other technologies have—leaving their overall effect on the economy more muted.

Is this theory a predictor of what will happen in the future? Certainly not. But one can think about the nature of value creation from advances in ICT. By and large, they have focused on automating routine activities. More modern innovations in AI and data science have focused on further, non-routine automation. These technologies key on reducing cost and price.

When labor is not able to use the gains from these efficiencies to focus on other, more value-added activities, the role of technology in GDP growth is challenged. As an anecdote, one rationale for the recent merger between Monsanto and Bayer is that farmers’ profit has not improved enough to continue to invest in GMO seeds. The point is clear: if our economy cannot find the kind of growth that creates a “rising tide for all boats,” we stunt the ability to bring new innovations to market.

Current business activity has a strong focus on protecting existing profit pools.

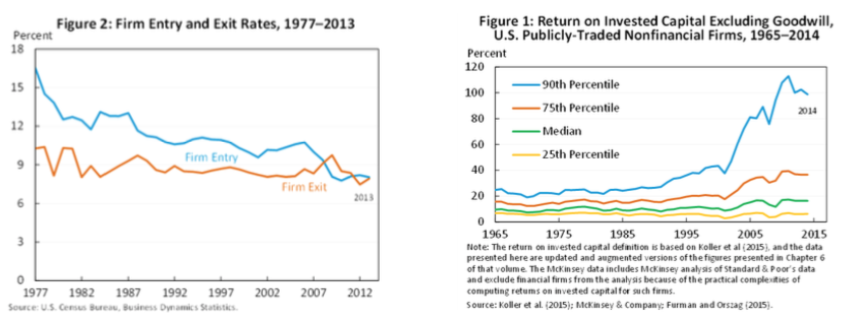

Disruptive technology should lead to a proliferation of new markets and/or significant churn in existing ones. However, this has not been the case: competition in the United States has slowed in recent decades. This has become a recent focus of the Council of Economic Advisors: ROIC is increasing (especially for market leaders), markets are becoming increasingly consolidated, M&A activity is increasing, and the rate of firm entry (startups) has been decreasing.

To wit: an American firm that was very profitable in 2003 (one with post-tax returns on capital of 15-25%, excluding goodwill) had an 83% chance of still being very profitable in 2013, according to McKinsey. In the previous decade the odds were about 50%. And since 2008, American firms have engaged in one of the largest rounds of mergers in their country’s history, worth $10 trillion.

Supporting this, incumbent businesses are using their resources to protect profit—and do so by investing in the continual modernization of their operations. These incremental investments in innovation (e.g., digitization) increase barriers for new entrants as organizations focus on their short-term profit. (Recent papers have noted a decline in basic and applied research within large corporations).

What does it all mean

Due to today’s market structures, dynamism and economic shifts will be slow without large shocks to competition. Digital skills will accrue most at incumbent firms, who have the resources to make investments and can create competitive moats. Public institutions should create incentives to spur investment into basic science R&D - we need leadership to focus on long-term sources of growth and diversify areas of productivity within the economy.

Additional research, perspective, and detail can be found in the following supporting articles:

- Intro: Creating a general framework for current opportunities and challenges.

- Part II: Aging & unproven learning models are headwinds to growth.

- Part III: Technology requires deeper integration into our work lives.

My goal in putting this together was to clarify my own thinking - and to present it in a way that can be challenged and deepened by others. I would be grateful to learn what may resonate (or differ) from your personal perspectives and work.